The Resource Blog

|

|

|

Part B giveback is another term for a Part B premium reduction or rebate. This is when a Medicare Advantage plan reduces the amount your client pays towards their Part B monthly premium. These rebates are offered by some Medicare Advantage plans and are designed to make plans more affordable. The amount of these Part B rebates can range depending upon the Medicare Advantage plan. They can be as low as $20 for some plans and yet, some plans offer more than $100 in giveback rebates.

How it Works:

If a Medicare beneficiary is on Social Security, the Part B premium comes out of their monthly benefit before the funds are deposited to their bank account OR it's reflected in their monthly check. The Part B giveback reduces their Part B premium, which means more money ends up in the individual’s bank account. If your client pays their Part B premium directly (not by automatic Social Security check deduction), their Part B premium statement will be updated with the giveback amount credited to what they owe. The standard Part B premium for 2024 is $174.70. This amount changes yearly and is based on income. An Example: If a beneficiary's monthly Social Security check is normally $1,600 and their giveback is $100, their Social Security benefit will now be $1,700. If they pay the standard Part B premium ($174.70) the amount they will owe after receiving the giveback will be $74.70. Part B givebacks can offer Medicare beneficiaries a way to save money by choosing a Medicare Advantage plan. To be eligible for this program your client must be responsible for paying their own Part B premium, which means they are NOT eligible to receive Medicaid or participate in a Medicare Savings Plan. As always, it's important to make sure a Medicare Advantage plan fits your client's needs and budget. It's also crucial to make sure it includes access to the doctors and hospitals they need, as well as making sure their prescription drugs are on the plan’s formulary.

No one wants to think that at some point in their life they're going to need someone to take care of them. We all like to think we'll be healthy, strong and capable for years and years to come. At some point we have to face the fact that we're going to get old and with that may come challenges. Discussing Long-term Care insurance with your younger clients is something to consider doing now. And we have a way to open the door to this conversation without them shutting it down.

70% of Americans over age 65 will need some sort of Long-term Care.

Ask your client to think about their parents and/or grandparents and their health. Ask them if they have family members who are utilizing Long-term Care services (Home Health Aide, Nursing Home, Assisted Living Facility); it will help make an impact on their decision to consider purchasing Long-term Care insurance.

If they give you the argument that their parents/grandparents are healthy and longevity runs in their family, you can acknowledge that, but then you can also point out the facts below if the statistic above doesn't nudge them:

If you need help with Long-term Care products or just have questions, please reach out to us. And if you're new to selling Long-term Care insurance, request our Getting Started with Long-term Care guide.

You're entering the world of Medicare solutions and you now have to select an FMO to work with, but how do you choose? When you Google 'Medicare FMOs' there's a long list and many are even sponsored. When it comes right down to it, FMOs are essentially the liaison between you and the insurance carriers you contract with. You have to go through an FMO in order to represent multiple carriers to your clients. If you don't, you'll have to look into becoming captive with an insurance company which will only allow you to sell their specific products. So back to your FMO research. Ultimately you need to find a partner who will be there to work with you to help you grow. Some important things to consider before placing all your contracts with one FMO are: longevity in the industry, selection of carriers and products, commission structure, education and training, marketing and sales support, quoting and enrollment tools, lead generation and finally back office support.

Below are some questions you should get answers to before placing your contracts with any FMO:

When you partner with an FMO that wants you to succeed, you're headed on a path for success. Do your research and be sure you get a good feeling about the organization before committing. The right FMO will fuel you with all the tools and resources you need to have a rewarding and profitable career.

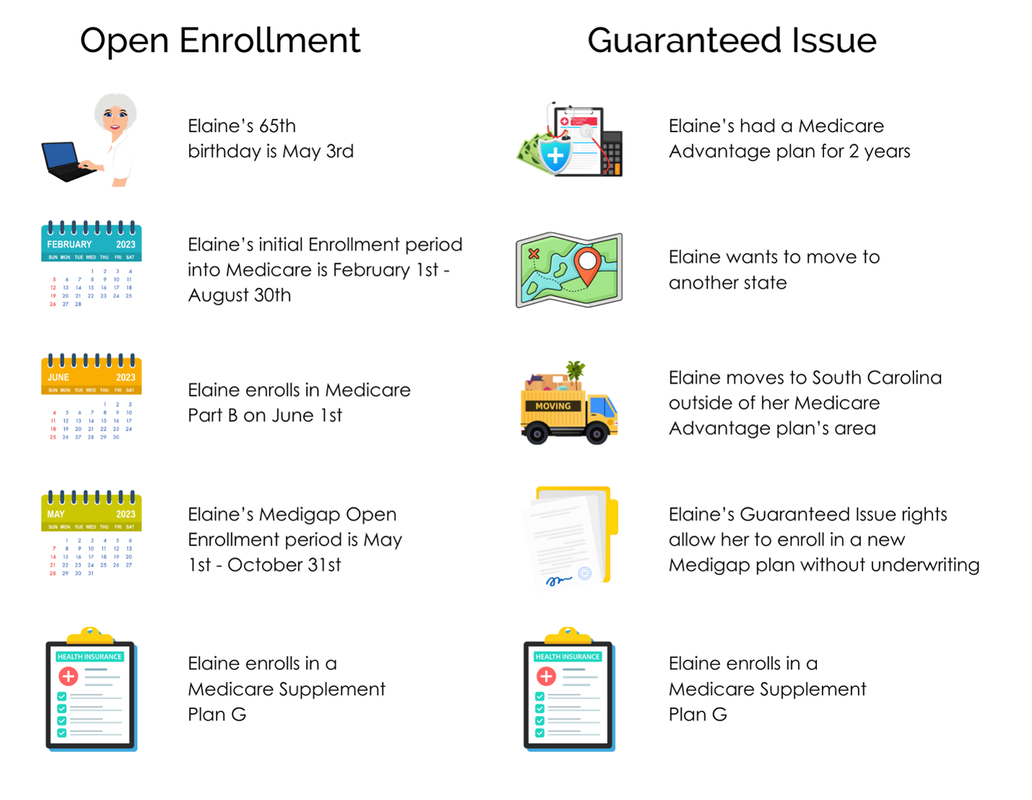

When it comes to Medicare Supplement policies there are times and situations when your client has the right to enroll in a Medigap plan without answering any health questions. The most important of those times being during their six month Medigap Open Enrollment period. This occurs when your client turns 65 or when they first enroll in Medicare Part B.

However, there may be times when you have a client who wants to enroll in a Medicare Supplement and they fall outside of their Open Enrollment period. Perhaps you have a client who's moving and they want to switch plans. Or you might have a client who was enrolled in a Medicare Advantage plan and they want to make the switch to a Medicare Supplement. Regardless of the situation, there may be Guaranteed Issue or Trial right available, allowing them to enroll in a Medigap plan without answering health questions.

Examples of Guaranteed Issue & Trial Rights:

Example: Same Client - Different Situations

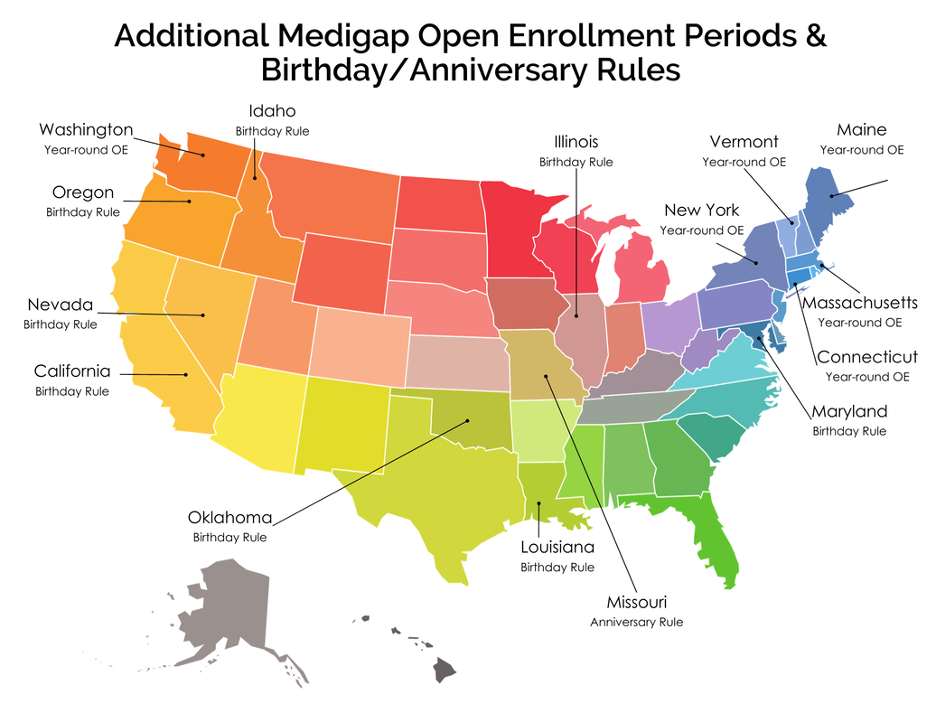

Year-round Enrollment & Other Rules

If your client doesn't fall under any of the Guaranteed Issue/Trial Right situations listed above, there are certain states that have year-round open enrollment periods. There are also states that have birthday and anniversary rules which allow your client to switch plans without going through underwriting. Each state has its own regulations and guidelines so it's important to familiarize yourself with them before enrolling your client in a Medicare Supplement plan.

If your client falls outside of their open enrollment period, doesn't live in a state with year-round open enrollment and doesn't qualify for guaranteed issue rights, they will likely have to go through underwriting; and that requires answering medical and pharmaceutical questions on the application as well as during a phone interview.

If you have any questions regarding Guaranteed Issue rights, birthday rules or getting your client through underwriting, please reach out to us and we'll be happy to assist you. Additionally, feel free to download our Medicare Enrollment Periods guide.

|